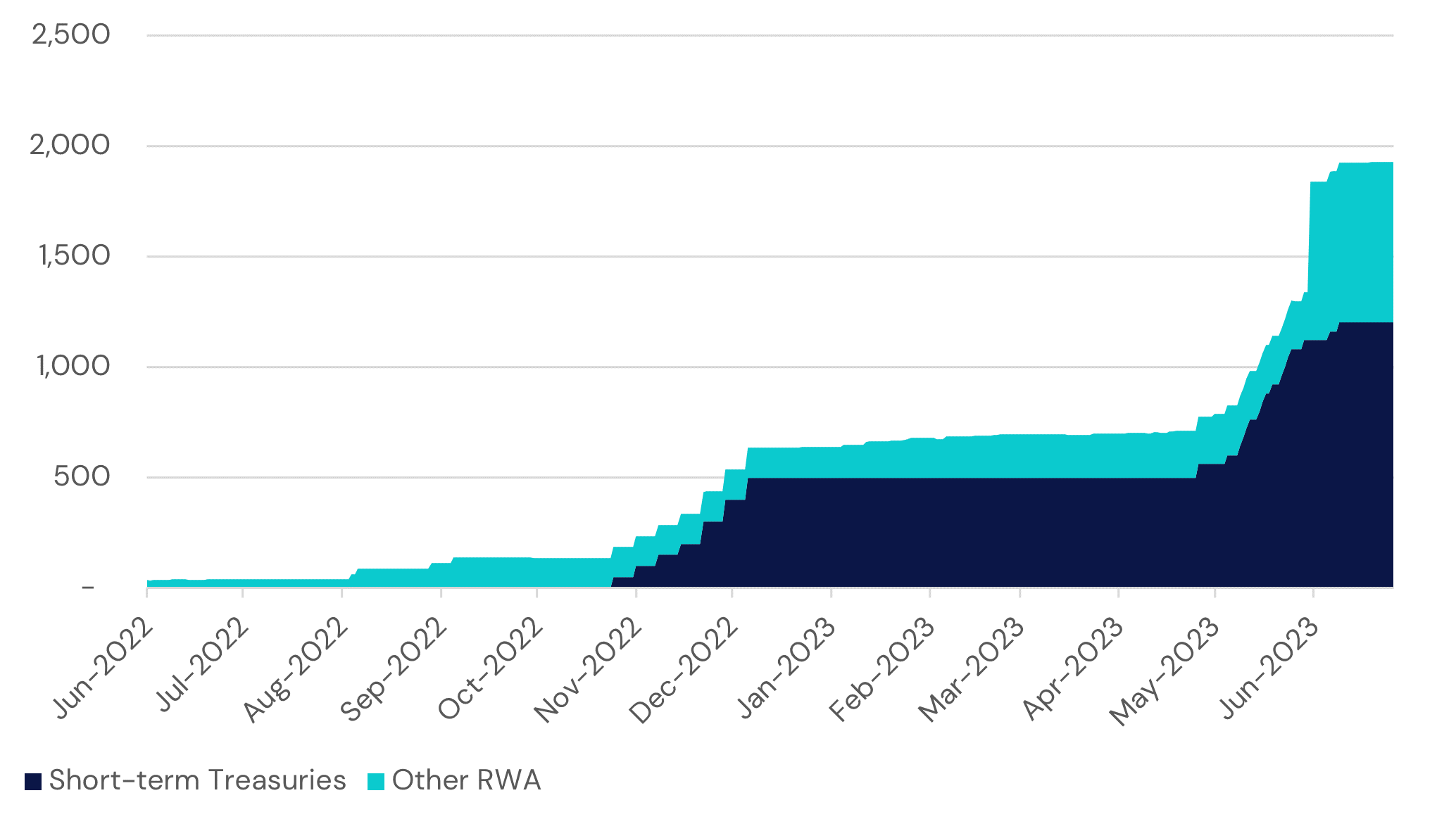

The tokenization of traditional financial assets has been hyped since the ICO boom of 2017. However, most of the necessary infrastructure to enable such a trend wasn’t developed until recently and the regulatory environment, while improving, remains murky. In good times and bad, Web3 maintains a community of builders who are willing to work, even when some foundational elements for scale are not yet in place. As such, we’ve seen a significant number of real-world assets (RWAs) represented on chain over the past couple years and MakerDAO has been leading the way.

Maker Real-World Assets (in millions, USD)

We’ve discussed the tokenization of traditional financial assets before. I’d thought this movement might be catalyzed through the introduction of liquidity to otherwise untraded instruments. Alternative investments, which are increasingly popular due to their differentiated sources of return, are seldom exchanged on secondary markets. Many projects continue to advance such initiatives, like offering digitized private credit in emerging economies, but these projects remain nascent and have seen smaller capital allocations than, say tokenized government debt.

Maker Real-World Assets (in millions, USD)

Maker’s case is a bit unique in that the real-world assets they represent on-chain form part of the collateral that backs their decentralized stablecoin, DAI. Given the importance of maintaining its peg to the USD, Maker has understandably less appetite for taking on credit or market risk in their portfolio, so an emphasis on short-term U.S. debt is sensible. However, they’re not alone in tokenizing T-Bills. Many institutional investors, including Franklin Templeton, have been flirting with bringing money market securities to blockchains. This comprehensive report digs into the current state of tokenized Treasuries and provides an overview of the projects available.

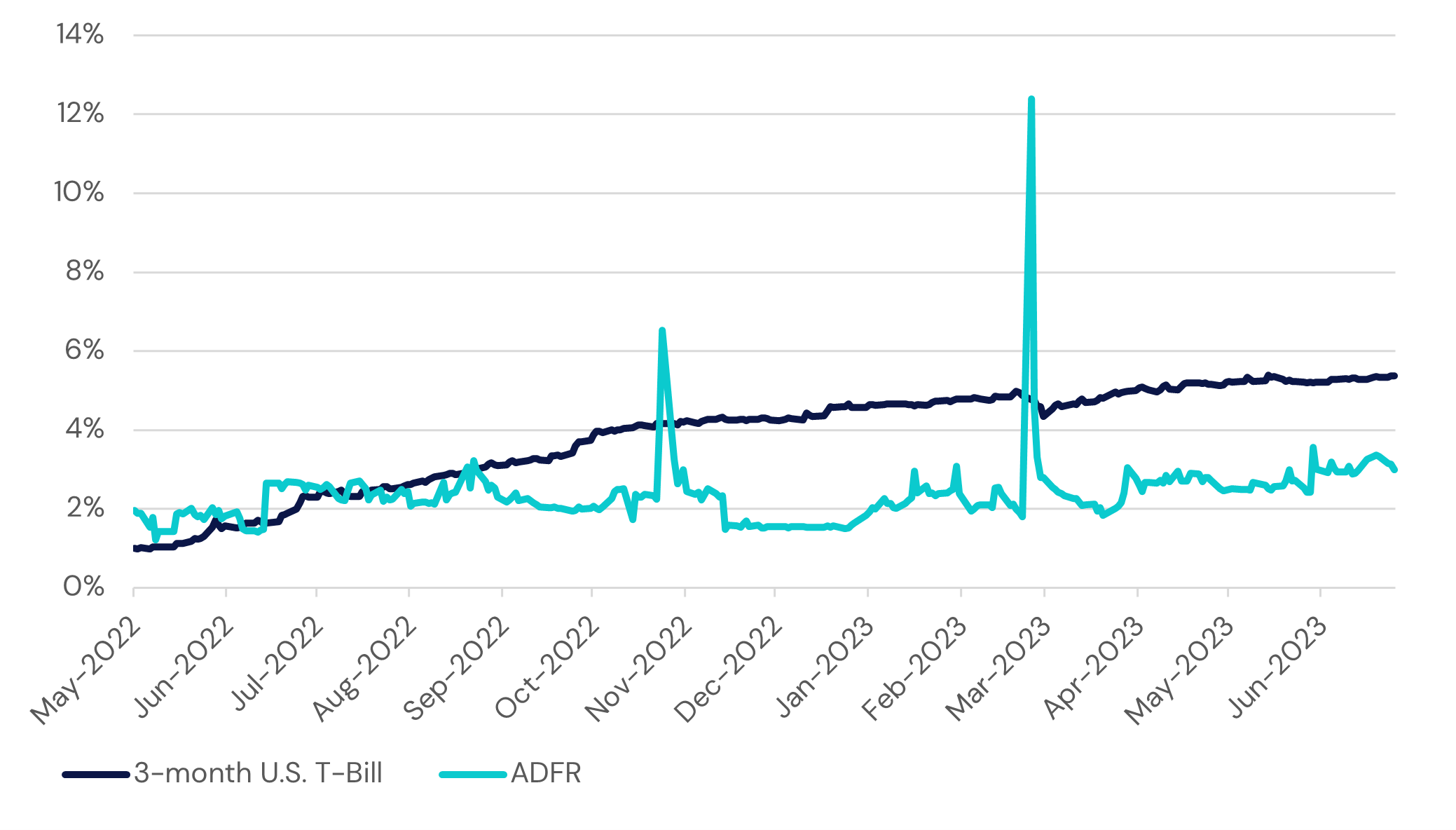

Today, most of Maker’s revenue comes from their portfolio of U.S. Treasuries. This outcome reflects profound macro shifts in both the traditional and digital economies. In the case of the former, central banks have increased policy rates at an unprecedented pace to combat rising consumer prices. Meanwhile, a massive deleveraging across the crypto landscape led to the exit of many investors, leaving a supply/demand imbalance of capital and projects. Somewhat ironically, the result is that the cost of capital in traditional (and generally less speculative) markets has surpassed what we see in Decentralized Finance (DeFi).

Interest Rates in DeFi vs. Traditional Markets

Back in the days of DeFi summer, some intrepid investors noticed that they could borrow capital at almost no cost in the “real world”, purchase stablecoins, and then lend those assets on venues like Aave and Compound. As compensation for taking smart contract risk, these pioneers were handsomely rewarded with interest and incentive tokens from the protocols, whose prices were rising rapidly. Things got a bit carried away though. Eventually a bubble formed, then burst, leading to the evaporation of billions from the crypto ecosystem.

Over the course of the cycle, the combined market capitalization of the most significant stablecoin projects rose dramatically, and while the level has come off its peak, over $100 billion remain represented 1:1 in the blockchain economy.

Combined Market Cap. of Major Stablecoins (in billions, USD)

For better or for worse, the largest stablecoin projects are centralized in nature. In the early days, the corporations behind the projects had to contend with many regulatory hurdles. Additionally, their underlying reserves were effectively earning no interest without taking on some credit risk. This meant that their main source of revenue was fees from minting and burning. Today’s macroeconomic environment is friendlier for stablecoin issuers, who are doing considerably better financially.

Robert Leshner is the founder and CEO of Compound, a decentralized money market protocol. After helping the project launch, he spearheaded Compound Treasury (CT) to take advantage of a significant disconnect between the rates of return offered in DeFi vs. traditional cash management venues. For nearly 15 years leading up to the current tightening cycle, interest rates were paltry, so returns on lending stablecoins stood out as relatively attractive. This is the opposite setup of today. CT launched as an innovative solution to bridge the gap between institutions and higher returns, even securing a credit rating from S&P. An allocation to the idea would have only suited companies with a high willingness to experiment, but it was an important advancement toward the goal of institutionalizing crypto. Unfortunately, the digital asset ecosystem began a dramatic deleveraging shortly thereafter, which effectively destroyed Compound Treasury’s business model.

I mention the story above because Mr. Leshner has demonstrated a passion for integrating blockchain technology and traditional finance. A few weeks ago, he announced his latest project, Superstate, which is said to be building “the future of compliant, blockchain-based financial products.” The first launch will be an SEC-registered short-term government bond fund.

Like some of the other products mentioned in the RWA.xyz report linked above, blockchain technology will be a part of the fund, but not central to its operation. At least not yet. The first versions of these tokenized Treasury funds are a bit clunky, but they’re a big step in the right direction.

For anyone interested in learning more about the intricacies of operating a compliant traditional asset fund on a blockchain, I’d recommend this conversation, which emphasizes that stablecoins are an important development, but that for some crypto users, giving up the ability to transact (more or less) permissionlessly can be offset by earning the yield of a stable asset like U.S. Treasuries.

Stablecoins emerged when interest rates were zero, so for believers of the underlying technology, the opportunity cost of holding USDC or USDT relative to a 1-month T-Bill was negligible. Now that policy rates have driven yields higher, we’re starting to see a new reflection of preferences. Say you have an investment strategy that switches between owning BTC and stablecoins depending on market conditions. Many traders aren’t concerned about satisfying the necessary KYC/AML requirements to own a fund that holds U.S. Treasuries. Instead, they’d prefer the 5% currently offered by these instruments. Regulated institutions are likely to be of this variety. As a result, they might be able to offer products with superior returns, but only to compliant investors.

Initially, the approach of Leshner and others may reduce the democratization potential of blockchains for some financial services, but as he notes “This is chapter one of — as a whole society and a whole industry — this shift of bringing assets on-chain.” Stablecoins are tokenized fiat, and they provide for the cheap and fast exchange of value. This is a killer use case that isn’t likely to go away. However, for some, the receipt of income neutralizes a slightly slower or controlled exchange of assets, and for those market participants we now have tokenized Treasuries. I still think the introduction of liquidity to alternative assets will be a powerful trend, but for now it seems that yield and stability supersede.

At Aquanow, we help institutions unlock the potential of digital assets, so if you or anyone you know are considering this functionality, then please get in touch. We’d be glad to leverage our expertise to help you outperform.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.