What a difference a year makes! While the Bitcoin chart suggests a bullish trend in the cryptocurrency markets, the remarkable surge in ETF flows—elevating digital asset prices to their highest in over two years—only reveals the initial layer of a much deeper narrative. It is the undercurrents within the stablecoin sector that weave a more compelling story. Significantly, in Y Combinator’s latest Request for Startups, the only mention of anything crypto-related is for “Stablecoin Finance”, which they see playing “a big part of the future of money.”

Digital asset markets are super reflexive, so higher prices beget more economic activity. Protocols generate more revenue, yields in the money markets move higher on margin lending, and people spend their gains on digital art.

After 18 months of declining market cap, the aggregate stablecoin value has recently inflected higher. This signals that outside capital is returning to the cryptosphere to partake in the activities above.

Total Stablecoin Market Capitalization (in billions, USD)

USDT remains the dominant stablecoin in terms of market capitalization and volume, largely due to its widespread use on cryptocurrency marketplaces, but also as a means of exchange in less developed economies. Its first-mover advantage has helped it maintain a strong position despite growing competition. USDC enjoyed a period of rapid market share growth, positioning itself as a leading stablecoin, especially among users seeking transparency and regulatory compliance. However, a risk management mishap brought to light during a mini banking crisis derailed the competitor’s momentum. The watershed moment underscored the complex dynamics and challenges within the stablecoin arena, where the balance between innovation, peg stability, access to banking, and regulatory relations remains a critical, ongoing battle.

USDT and USDC Market Capitalizations (in billions, USD)

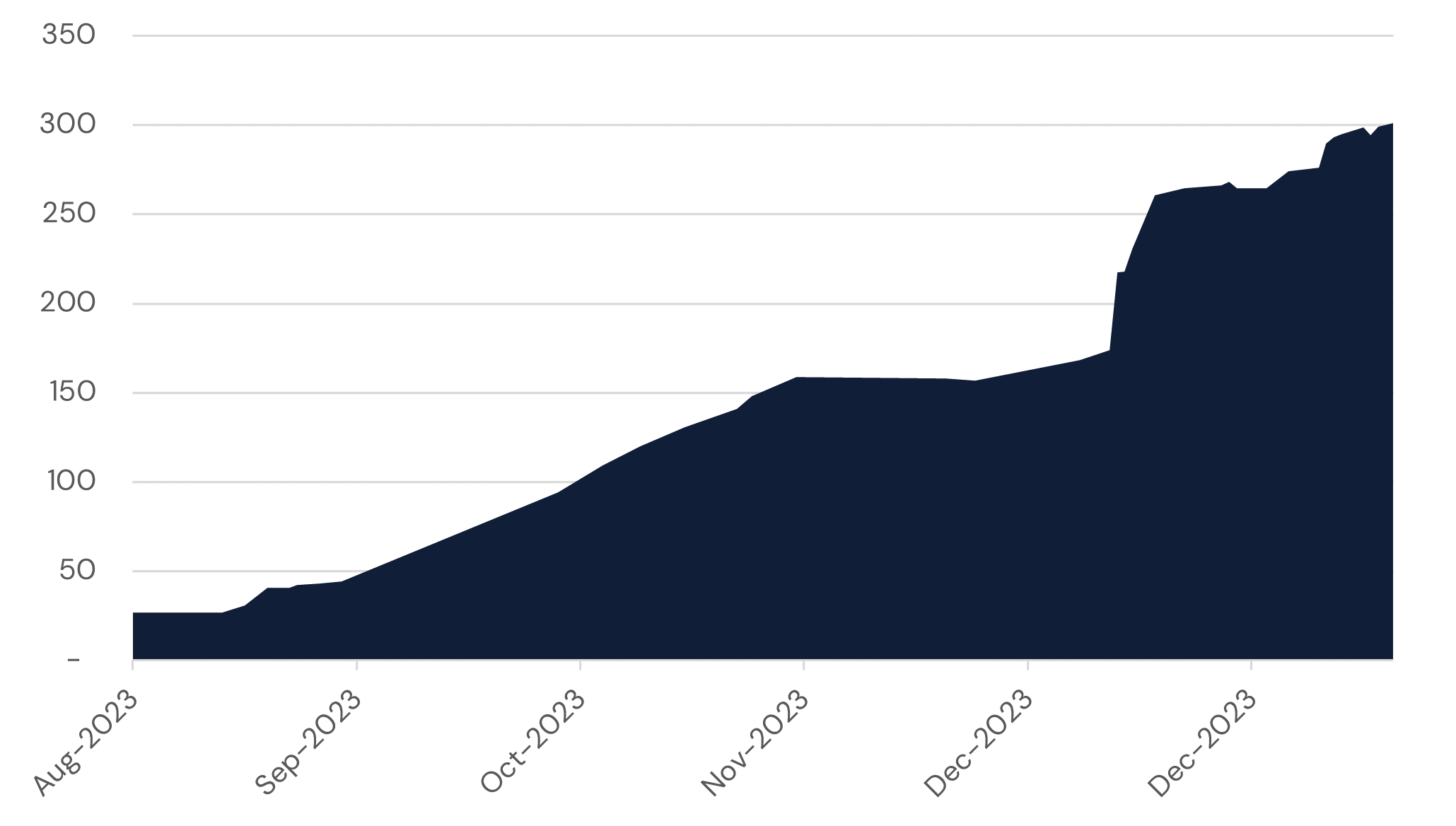

PayPal's PYUSD is a newcomer to the stablecoin market, and while it does not yet have anywhere near the market share of USDC or USDT, PayPal's vast user base and established presence in online payments could accelerate its adoption significantly. PYUSD is expected to leverage its sponsor’s existing technological infrastructure, which is known for its robust compliance and security measures. Increasingly, the token has been making its way into DeFi. First as a component of pools on Curve, and just this week as an asset on Aave.

PYUSD Supply (in millions, USD)

Recently, the stablecoin ecosystem has witnessed a series of significant announcements, further solidifying the idea that blockchain-based currencies are becoming increasingly integral to the financial landscape.

Tether’s latest reserves report boasted a quarterly profit of $2.85B and annual asset growth of 45%. It’s also worth noting that the company’s credit risk profile has improved substantially, reducing its commercial paper exposure in the cash segment of the balance sheet to zero in 2023. Tether's strategic move to lead Oobit’s $25 million Series A funding round is part of a meaningful push to integrate stablecoins into everyday commerce. Oobit's innovative solution enables crypto holders to use their digital assets for Tap & Pay transactions at over 100 million retailers worldwide that accept Visa and Mastercard, bridging the gap between traditional finance and digital currencies.

Crypto market observers are set to receive even more transparency into the financials of operating a stablecoin issuer as Circle filed an IPO prospectus confidentially. This is the company’s second shot at going public after its attempt to list via SPAC fell apart a year ago. There are many interesting components to this story. Going public requires stringent regulatory compliance and financial transparency, which could enhance trust in USDC (and stablecoins in general) among equity market participants. The publicity and financial backing from an IPO could also ease Circle’s global growth ambitions. Finally, with additional capital, the company could invest in new technologies and partnerships, potentially leading to more use cases for USDC in payments, settlements, and DeFi.

Circle’s partnership with Solana Pay was highlighted recently. Anatoly Yakovenko, the co-founder of Solana Labs disclosed that Solana Mobile did $20M in sales through Shopify and 51% of users self-selected to pay with USDC, saving over $600K in credit card processing fees.

Now, the average purchaser of a Solana mobile phone is likely crypto-native, so the sampling bias here is high, but the savings are legitimate. Therefore, you can imagine others will catch on and provide discounts to USDC payers. However, another fascinating development in the economics of stablecoin issuers is that Circle will soon be levying a 0.1% fee on redemptions above a certain threshold. Small businesses will still be able to withdraw for free, but it’s an interesting departure from previous strategy, especially given the demonstrated profitability at Tether (who always charges a 0.1% fee) and the upcoming IPO. Some have also speculated that costless redemptions and Circle’s advantage in access to onshore banking have made USDC a sort of de facto off ramp as operators looked to pay bills in fiat from revenues earned in crypto. Adding this friction might be a way for Circle to profit without losing (and perhaps even gaining) relative market share!

In a way, there’s already a Nasdaq-listed stablecoin issuer, but the segment is too small to warrant its own segmentation in PayPal’s financial statements. I was hoping to glean some intel on PYUSD from the company’s year-end reporting, but the asset wasn’t mentioned. However, this may be by design given the SEC’s continued adversarial stance towards crypto more broadly and the vehement opposition to Facebook/Meta’s attempt at a stablecoin. If you read the company’s latest areas of focus, it's not hard to imagine PYUSD fitting in nicely.

Enhanced profitability and payment/checkout innovation were obvious themes in PayPal’s latest disclosures, so given Tether’s profitability and USDC’s recent success on Solana, the company may be well-served to lean into its stablecoin offering. Lo and behold, PayPal Ventures announced a $5 million PYUSD allocation to Mesh, a sort of Plaid for crypto. This intrepid investment not only fuels Mesh's growth ambitions but also serves as a significant endorsement of the practical utility, growing acceptance, and sponsor commitment of stablecoins more broadly.

Stablecoins are most interesting because they’re non-speculative by nature. As such, they serve as a pureplay on programmable money, highlighting the technological components of crypto. The strategic moves by Circle, Tether, and PayPal, along with the evolving regulatory and technological* landscape, will significantly influence the future of the stablecoin market. While challenges remain, the potential for these assets to transform finance is immense. The coming years will likely see these stablecoins expand their reach, innovate their offerings, and possibly redefine the boundaries between cryptocurrency and traditional financial systems.

*If you made it this far, then I think you should read this whitepaper

Aquanow helps money transfer businesses lower their costs. Contact us to explore how our expertise can enhance your performance.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.