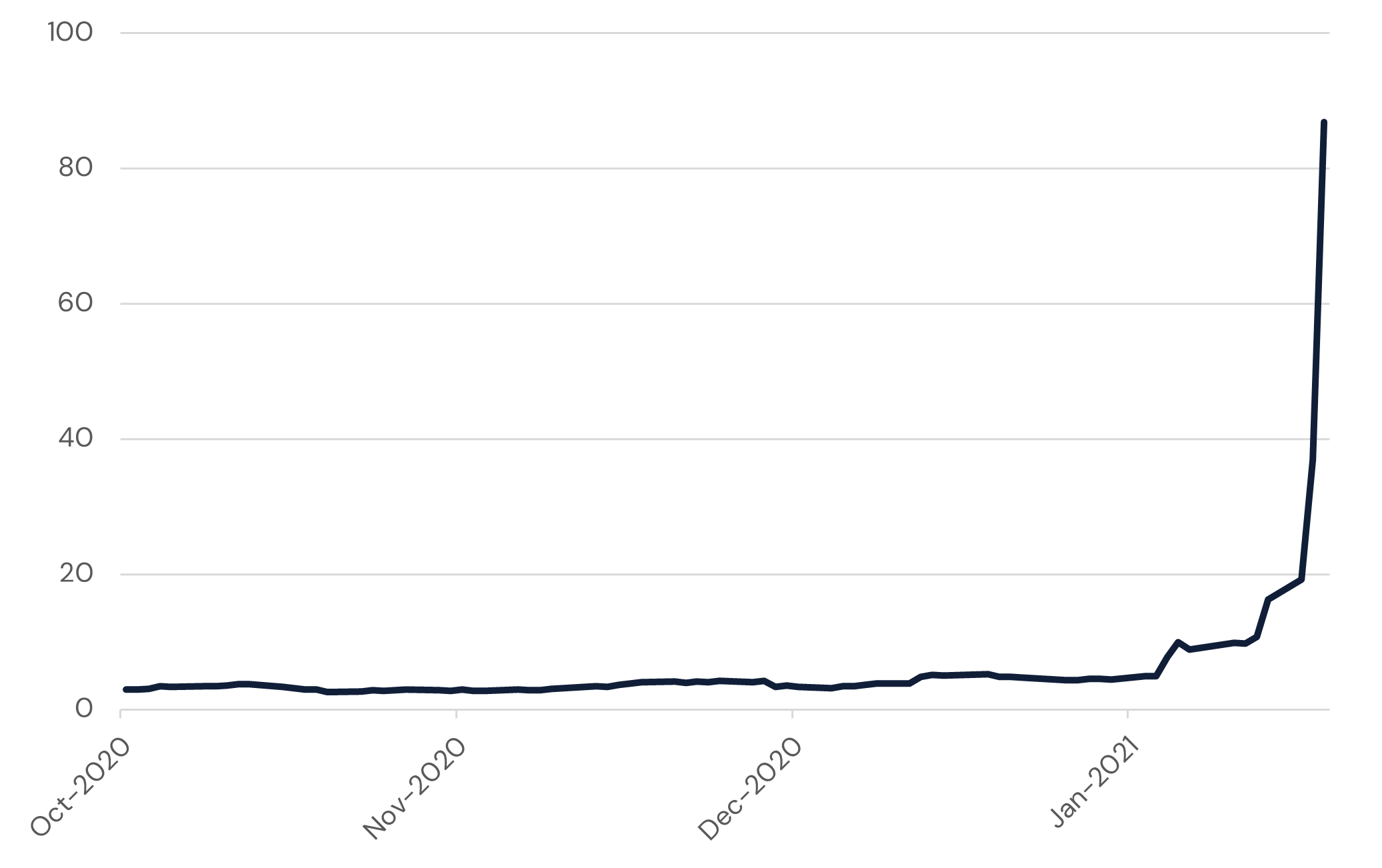

Three years ago, the global financial markets were abuzz with a dramatic new force in U.S. equities. Viral collective bullishness from retail traders on YouTube, Twitter (now X), and Reddit’s Wall St. Bets combined with a massive short interest sent the stock of the fledgling retailer, GameStop (GME), to the stratosphere.

GameStop Corp. (GME – NYSE) Stock Price

This “meme-stock” phenomenon was the first demonstration of social media’s power in the investment decision-making process at global scale. GameStop’s equity price rose dramatically but caused significant losses for hedge funds that had to cover short positions. Although some did profit from the event, researchers have shown that GameStop investors increased their exposure to default risks, regulatory uncertainty, and online misinformation. Depending on the timing of one’s purchase, the returns are dramatically different as well. The shares are down 84% since their peak, but still sit roughly 3x higher than before the drama.

As you may have seen in the movie Dumb Money, a key figure in the GME story was an online personality who operated under the pseudonym of Roaring Kitty. Keith Gill is a financial analyst and investor who gained significant media attention during the 2021 GME short squeeze. While there have been many stock market celebrities in the past, Gill’s social media fame make him one of the world’s first “finfluencers”.

Just as social media personalities have become a key vehicle to promote products and services for brands, finfluencers are emerging as pivotal intermediaries in the financial services sector, offering investment information, product promotion, and even security recommendations. Their growing impact is particularly notable among young investors, a cohort set to see its economic power rise meaningfully in the coming years. Regulators have taken note, and platforms have policies in place to curb certain behaviours, but there remains considerable grey area regarding online characters’ authorization to engage in otherwise regulated financial activities.

Last week, the CFA Institute (CFAI) published a report called “The Finfluencer Appeal: Investing in the Age of Social Media” and it’s a good read for anyone involved in financial markets. As of 2023, there are 4.8 billion social media users worldwide, representing 60% of the global population. These relatively new platforms have revolutionized how the world stays in touch and have profoundly impacted the flow of investment information. Anyone with an internet connection can now leverage network effects to access current events, learn about market structure, and deepen their industry knowledge.

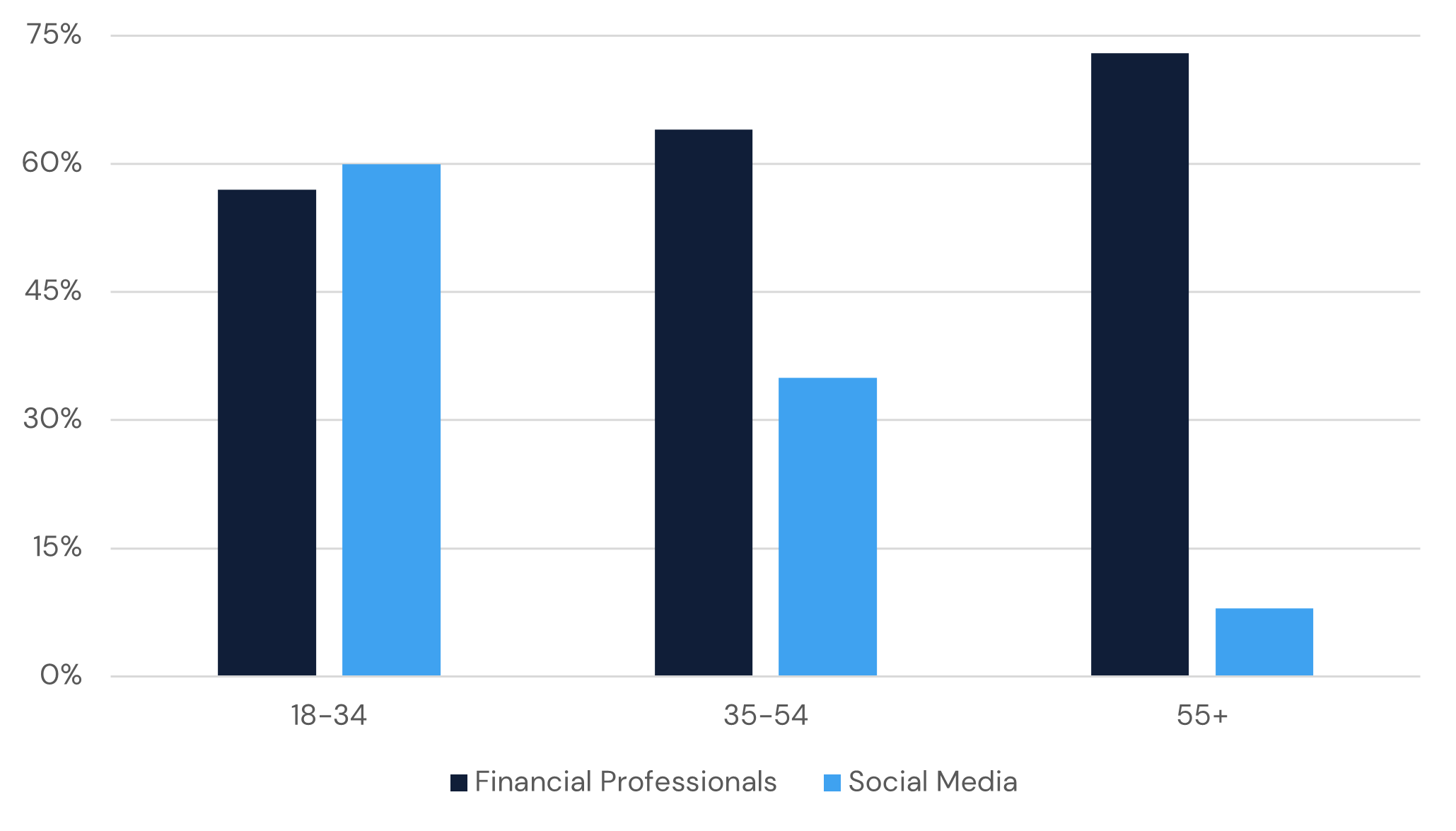

The trend in sourcing investment insights through social media is particularly pronounced among different age groups. A FINRA analysis found that 60% of U.S. investors aged 18–34 rely on social media for their portfolio insights, in stark contrast to 35% of those aged 35–54 and a mere 8% of the investing population aged 55 and older. This demographic difference underscores a growing divide in how different generations approach portfolio research and decision-making, with younger investors increasingly turning to digital platforms for guidance and knowledge.

Sources of Investment Information Used by Age Group

According to the CFAI report, a primary issue is that many finfluencers operate without regulation, leading to potential risks for their audience. Additionally, there's a tendency among viewers to equate a finfluencer's follower count with their credibility, which may not always be a reliable indicator of their expertise or trustworthiness. The paper also notes that finfluencers can sometimes make dubious recommendations, further complicating the reliability of the information they provide. Underlying these issues are strong potential conflicts of interest, particularly regarding the compensation received for promoting specific products and services, which could bias the impartiality of their advice.

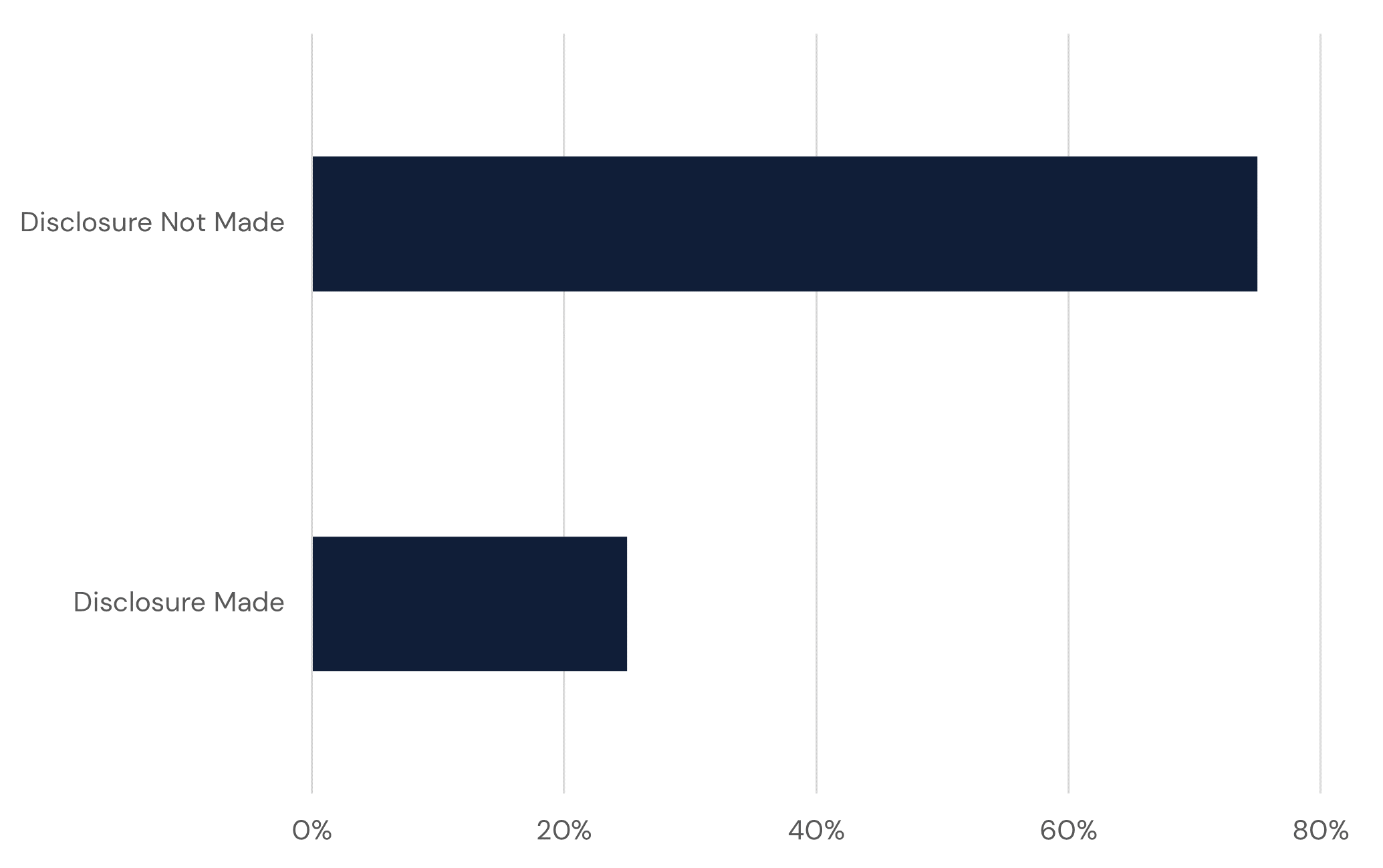

Much like in the broader markets, social media is a driving force in digital assets. In fact, its prominence is exacerbated due to the tendency of blockchain enthusiasts to be younger and technologically inclined. While they offer valuable insights and democratize financial knowledge, crypto finfluencers are mired in controversy. Like the GameStop incident, where social media-driven investing led to unprecedented market volatility, crypto influencers have been known to promote projects without sufficient vetting, leading to scams and financial losses for uninformed investors. I love watching digital asset interviews on YouTube and while I know that “not financial advice” implies an opinion that requires additional due diligence, many ignore such warnings, if they’re given at all.

Proportion of Content That Contained Disclosures

The main differentiators of professional advisors vis à vis finfluencers are that the information they provide can be tailored and comes with assurances of quality, professional competency, and duty of care. Furthermore, there are standards and regulatory bodies that enforce compliance. Advisors must emphasise these elements in their value proposition if they are to stay competitive in an increasingly digitalised world. Critically, many of these advisors were/are against crypto which is both out-of-touch and in many cases has been expensive in terms of opportunity cost. However, the recently approved spot Bitcoin ETFs provide a relatively easy path to incorporating digital assets into portfolio construction conversations, so we’ll see if advisors can win back some trust relative to talking heads on social media.

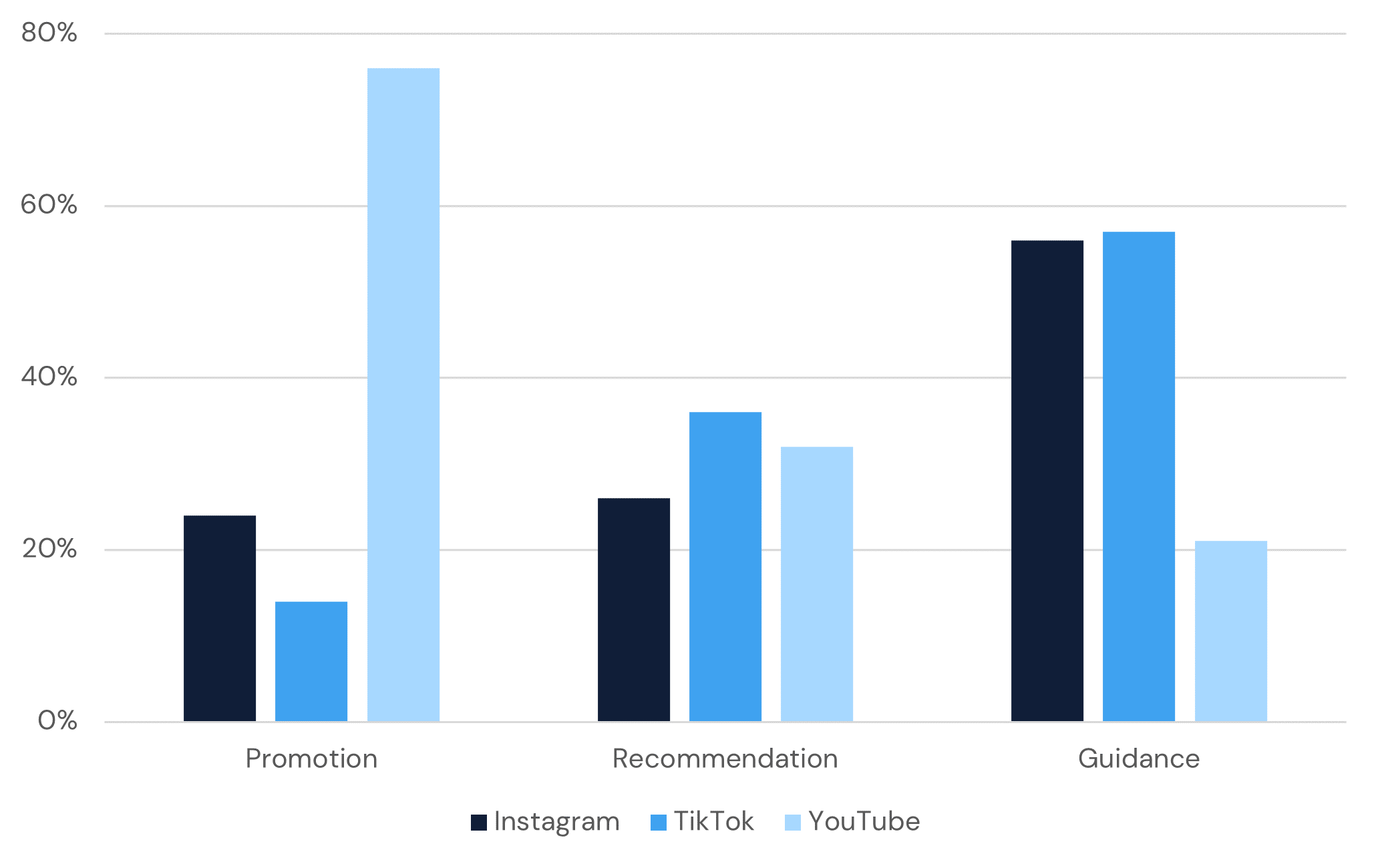

Promotions, Recommendations, and Guidance by Social Media Platform

The CFAI researchers suggest that regulators across various jurisdictions should collaborate to establish a more universal and clear definition of what constitutes an investment recommendation. This would help in setting consistent standards and expectations. Additionally, the findings recommend that national regulators proactively engage with finfluencers, fostering a better understanding and compliance with financial regulations. Furthermore, it's advised that watchdogs maintain and publicly share data regarding complaints and whistle-blowing activities related to finfluencers. This transparency could play a crucial role in monitoring and addressing any problematic practices within this emerging field. All of this sounds a lot like the kind of regulation that the digital asset lobbyists have been asking for the industry more broadly too… Being a policy maker is tough in the exponential age.

The rise of finfluencers marks a significant shift in the landscape of financial advice and investment strategies, particularly in the digital age. As the CFA Institute's report and other studies highlight, the dominion of social media on investment decisions is undeniable, especially among younger generations. While finfluencers democratize access to information often ignored by curriculums and can offer fresh perspectives, their unregulated nature and potential conflicts of interest pose challenges to the integrity and reliability of financial advice disseminated online. The GameStop saga and the volatile nature of cryptocurrency investments underscore the risks associated with following unvetted advice. This is a theme worth paying attention to.

Aquanow specializes in unlocking digital asset potential for financial institutions. Contact us to explore how our expertise can enhance your performance.

If you want to contribute to the web3 movement, Aquanow is on the look for curious and motivated folks to join our team. Feel free to reach out directly or check out the current openings here.